With the adoption of IFRS 16 on 1st January 2019, calculating the free cashflow for some firms has gotten quite a bit trickier with several pitfalls to be navigated depending on the individual case – let’s take a look.

What happened?

Simply put, under IFRS 16 a company has to recognize leased assets on its balance sheet (as a right-of-use asset with a corresponding liability) if it has control (or the right to use) of said asset. In the past, these leases (so called operating lease) were usually carried off-balance sheet.

For companies that make use of a substantial amount of longer term leases the implementation of IFRS 16 can cause quite a bit of change to the balance sheet, P&L, and also the cash flow statement. To be clear: The actual cash flows paid on these lease contracts do not change, however their accounting treatment and presentation does.

Changes to the balance sheet and profit & loss statement

Without going into too much detail, the balance sheet expands since the long-term leases are recognized as an right-of-use asset on the asset side of the balance sheet. Correspondingly, a lease obligation is recognized on the liability side. This impacts the profit & loss statement (P&L) as well: Whereas in a pre-IFRS 16 world one would have simply seen a lease or rent expense in the P&L equal to the actual periodic lease payment, this is now replaced by a depreciation of the newly recognized right-of-use asset as well as an assumed interest expense on the lease liability. This all sounds pretty complex and slightly confusing, and it is at first glance. Take a look the following set of numbers presented by Brenntag, the worlds largest chemical distributor for fiscal year 2019:

| in EURm | 2019 | 2018 |

| EBITDA | 992.9 | 858.1 |

| Depreciation | -243.6 | -122.0 |

| Amortization | -49.6 | -49.9 |

| EBIT | 699.7 | 686.2 |

| Financial result | -83.5 | -97.5 |

| EBT | 616.2 | 588.7 |

At first glance an increase in EBITDA of 134.8m EUR or 15.7 % looks impressive, however depreciation expenses increased by a similar amount, almost offsetting the increase on an EBIT level. This effect is almost entirely due to the company adopting IFRS 16 for the first time in 2019. EBITDA figures can hence be a misleading indicator under IFRS 16, especially when compared to pre-IFRS 16 numbers. Now let’s look at the cash flow statement.

Calculating free cashflow under IFRS 16

Normally, calculating free cashflow is a straight forward matter: We simply deduct the cash paid for property, plant and equipment as well as intangibles (short “CAPEX”) from the operating cashflow et voilà: we have our free cashflow figure. However, under IFRS 16 this changes slightly for two reasons:

- The cashflow from operating activities will be “overstated” given the increase in depreciation

- Parts of the lease payments might be accounted for in the cashflow from financing activities as a repayment of debt

Let`s take a look at these points using the aboved mentioned example of Brenntag. First off the operating cashflow. Here we see a strong increase from 375.3m EUR to 879.3m EUR, which is partly explained by much better working capital management in 2019, but also by the increase in depreciation due to IFRS 16:

The cashflow from investing activities does not change materially due to IFRS 16, in this case the CAPEX can be taken directly from the cash flow statement at -204.0m EUR:

Normally, we would simply calculate the free cashflow for 2019 as 879.3m EUR minus 204.0m EUR and be done at this point. However, this is where IFRS 16 creates an issue: As can be seen in the excerpt of the operating cashflow above, the application of IFRS 16 clearly increased that number. Hence something gotta give – in this case, the cash flow from financing activities:

Included in the 290.2m EUR of repayments of borrowings are 120.7m EUR of lease repayments. How do we know? – Unfortunately this number can not be found in the financial statement, but Brenntag discloses the figure thankfully in the descriptive part of the annual report.

Summing it all up the new free cashflow figure can be derived as 879.3m EUR – 204.0m EUR – 120.7m EUR = 554.6m EUR.

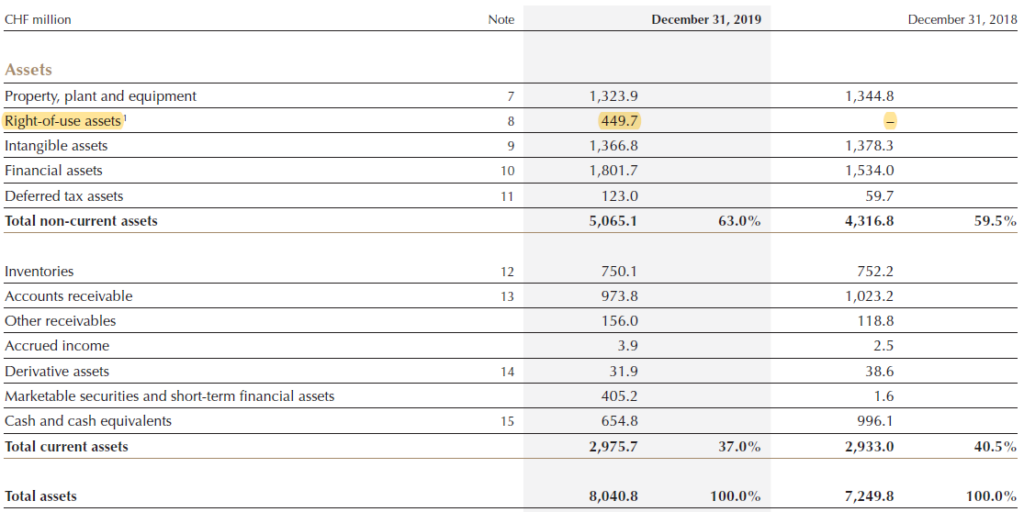

Not all companies financial statements are affected to this degree by IFRS 16 and some also provide more information to easier assess the impact. Lindt & Sprüngli’s balance sheet for example clearly shows an impact from IFRS 16:

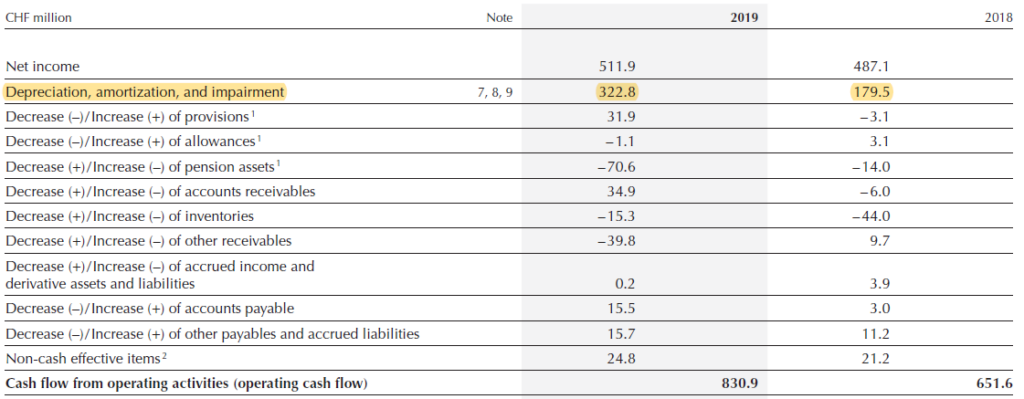

And so does its cashflow from operations with a corresponding increase in depreciation:

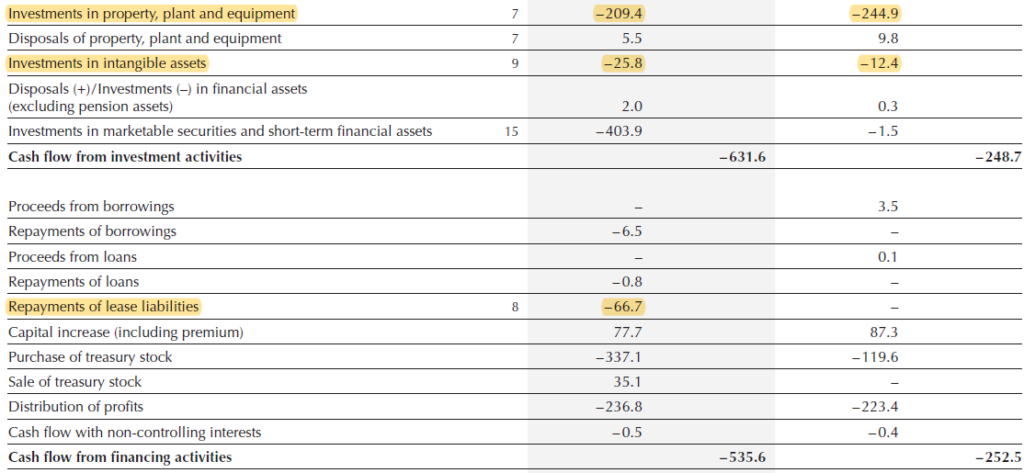

However, the company makes it easy to properly calculate its free cashflow by providing the lease liability repayment as a separate line item in its cashflow from financing activities:

Accordingly, the free cashflow amounts to 529.0m CHF (830.9m CHF – 209.4m CHF – 25.8m CHF – 66.7m CHF).

The bottom line

The main takeaway is that the introduction of IFRS 16 changes the calculation of free cashflow figures since (contrary to the usual approach) repayments on lease liabilities have to be taken into account. On the other hand, IFRS 16 will have little impact on companies that do not make use of a substantial amount of longer-term leases for which the changes are negligible.